Heat Exchangers Market [By Product Type (Shell & Tube (U-Tube, Straight Tube (1 & 2 Pass Tube Side)), Plate & Frame (Gasket, Welded, Brazed), Air Cooled, Extended Surface, Heat Sinks, Regenerative, Printed Circuit (PCHE)); By Material of Construction (Carbon Steel, Stainless Steel, Nickel, Others); By Graphite Heat Exchanger (Cubic, Graphite Block, Polytube Graphite Shell & Tube Block); By Application Type (Pulp & Paper, Automotive, Healthcare, Chemical, Electronics, Petrochemicals and Oil & Gas, Food & Beverage, HVACR, Others), By Regions]: Market size & Forecast, 2018 – 2026

- Published Date:Aug-2018

- Pages: 211

- Format: PDF

- Report ID: PM1355

- Base Year: 2017

- Historical Data: 2015-2016

Report Outlook

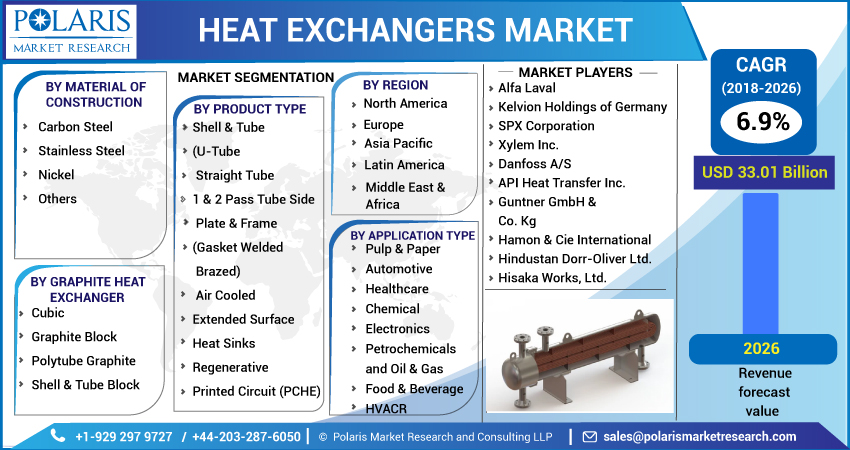

The global Heat Exchangers market is anticipated to grow at a CAGR of 6.9% between 2018 and 2026. The global industry has witnessed significant demand growth in the past few years and is expected to continue to grow on account of rapid industrialization across many parts of the world. Chemical, petrochemical, automotive, HVAC, and food & beverage industries are among the top end-use industries driving the global demand for this equipment.

The countries in North America and Europe such as the U.S. and Germany respectively have generated a profitable market for heat exchangers. However, the growth in per capita consumption income in countries such as China, India and the developing countries of Southeast Asia (Indonesia, Vietnam, and others) has led to rigorous industrial development which in turn has positively influenced the demand of these equipment.

The industry, coupled with the above-mentioned drivers is strongly driven by the growing demand for energy efficiency and reduced carbon emissions. Increasing consumer preference for energy-efficient and smart products (buildings & electronic devices) has helped evolve the heating equipment market in a very technologically advanced way.

Government support & initiatives across different regions and countries have played a significant role in taking heat exchangers towards energy-efficient end-use industries. New efficiency norms by agencies such as Office of Energy Efficiency and Renewable Energy (DOE), Paris Summit, and country-level energy commissions have extensively introduced mandates regarding smart construction & manufacturing in the industrial, commercial, and residential sectors for a sustainable environment.

A heat exchanger is a device that transfers heat between two or more fluids at varied temperatures. The fluids are separated by a wall having high thermal conductivity. The thickness of the wall is designed such that the fluids don’t mix or come in direct contact. Heat exchangers differentiate themselves from fuel, nuclear, or electrical heat transfer equipment. Here, the heat source and receiving medium need to be both fluids. Heat exchangers operate using thermodynamic principles, describing the transfer of thermal energy at the macroscopic level.

Heat exchangers are mainly classified based on their flow configuration and construction type. The most basic heat exchanger involves the movement of cold and hot fluids in the same or opposing directions. Based on their functionality, heat exchangers can be classified as recuperative heat exchangers, regenerative heat exchangers, and direct mixing type heat exchangers. These exchangers have a wide variety of applications in several sectors, including chemical plants, petrochemical plants, power stations, and petroleum refineries. Besides, heat exchangers in the heat exchangers market also find applications in IC engines, where they promote the flow of engine coolants through radiator coils as air flows past them.

Segment Analysis

The global heat exchanger market has been segmented on the basis of product types, materials used for manufacture of these equipments and its end use industries. The product segment is further bifurcated into shell & tube, air cooled, plate & frame, extended surface, heat sinks, regenerative and printed circuit (PCHE).

Shell & tube heat exchangers are further bifurcated into U- tube, straight tube (1 and 2 pass tube side). Graphite made shell & tube heat exchangers are further bifurcated into cubic, graphite block, polytube graphite heat exchangers.

Plate and frame product segment is further segmented into gasket, welded and brazed heat exchangers. In terms of materials used for construction of these equipment the market is further subdivided into carbon steel, stainless steel, nickel and others. The end use industries segmented into pulp & paper, automotive, healthcare, chemical, electronics, petrochemicals, food *& beverage, HVACR and others.

Shell & tube exchangers were the largest product types in 2017. These are one of the most widely used heat exchanger for industrial applications. These are generally selected for applications such as hydraulic & lube cooling, compressor & engine cooling, in heat recovery for thermal energy conservation efforts, process gas or liquid cooling, refrigerant vapor and steam condensing.

Regional Analysis

Asia Pacific segment accounted for the majority share of the global market in 2017. The region is expected to hold over thirty percent of the total global industry over the next nine years. Asia Pacific region’s increasing manufacturing industry size, developing chemical, oil & gas, petrochemical setors are among the major contributors to product demand.

Rising construction projects in industrial and commercial establishments are expected to drive HVAC market in the region. Constructive regulatory strategies in Japan and India to develop solar and thermal energy are projected to drive product demand in the power generation industry in the region. Growing need for heat recovery applications in HVAC, chemical and food & beverage manufacturing industry is anticipated to drive these equipments demand in the region.

Competitive Analysis

Some of the leading industry participants include the Alfa Laval, Kelvion Holdings of Germany, SPX Corporation, Xylem Inc., Danfoss A/S, API Heat Transfer Inc., Guntner GmbH & Co. Kg, Hamon & Cie International, Hindustan Dorr-Oliver Ltd. and Hisaka Works, Ltd.